How do you save your money?

Some people keep it in the bank.

Some invest it in stocks.

Some just hope their paycheck keeps growing.

But if we’re honest, many people are doing the financial equivalent of burying money in the backyard.

Maybe not literally—but financially speaking, it’s not that different.

The real question isn’t just how much you save.

It’s how hard your money works after you save it.

Some strategies protect your money.

Some grow it.

Some produce income.

Understanding the difference can completely change your financial future.

Let’s walk through five common ways people save or invest their money—from the safest to the most interesting.

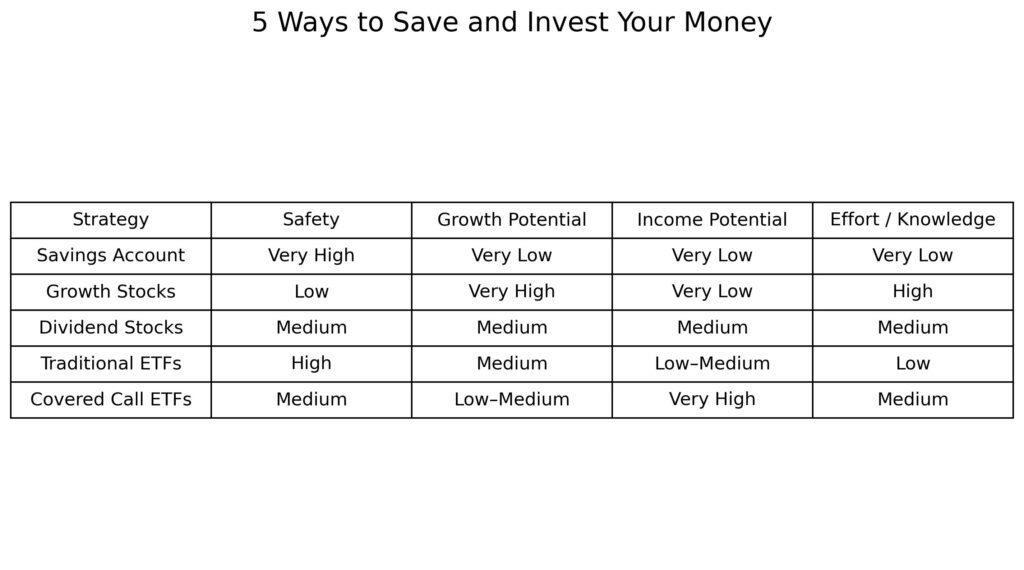

1. The “Sleep Well” Strategy: Savings Accounts

The most common place people keep their money is a savings account.

Banks pay you interest for keeping money there.

For example:

- Deposit: $10,000

- Interest rate: 4%

- Annual earnings: about $400

Sounds reasonable, right?

Not quite.

The hidden problem is inflation.

Inflation is the steady rise in prices over time. If inflation is 3–4% per year and your savings earn 2–4%, your money may barely keep up—or even lose purchasing power.

In simple terms:

Your money grows…

but what it can buy shrinks.

Savings accounts are great for emergency funds and short-term cash, but they are rarely effective tools for long-term wealth building.

Think of them as a parking lot for money, not an engine for growth.

2. The “Swing for the Fences” Strategy: Growth Stocks

Now let’s talk about growth stocks.

When you buy a stock, you’re buying a small piece of a company.

Growth companies are businesses expected to expand quickly. Instead of paying cash to shareholders, they reinvest profits into things like:

- hiring employees

- building new products

- expanding into new markets

Investors buy these stocks hoping the price rises dramatically over time.

Example:

- Buy a stock at $100

- The company grows for years

- The stock eventually reaches $500… or even $1,000

Some famous growth stocks have increased hundreds or thousands of percent over time.

But there’s a catch.

Growth stocks can also drop sharply.

Prices can swing wildly based on economic conditions, company performance, or investor sentiment.

This strategy rewards patience—but it also requires research and emotional discipline.

3. The “Get Paid to Wait” Strategy: Dividend Stocks

Some investors prefer a different approach.

Instead of waiting for prices to rise, they invest in companies that pay them cash regularly.

These are called dividend stocks.

A dividend is a portion of a company’s profits distributed to shareholders.

Many mature companies—especially in industries like utilities, consumer goods, and energy—pay dividends every quarter.

Example:

- Stock price: $100

- Annual dividend: $4

- Dividend yield: 4%

That means investors earn 4% per year in cash payments, regardless of whether the stock price changes.

This strategy appeals to investors who want passive income.

But there’s an important rule in dividend investing:

Don’t chase yield.

If a company is paying extremely high dividends, investors must ask why. Sometimes high yields indicate financial stress rather than strength.

Dividend stocks can provide steady income—but they usually grow more slowly than aggressive growth companies.

4. The “Set It and Forget It” Strategy: ETFs

For many investors, the simplest and most reliable strategy is Exchange Traded Funds (ETFs).

An ETF is essentially a basket of many stocks combined into one investment.

Instead of trying to pick individual winners, ETFs allow investors to buy an entire segment of the market.

Popular examples include:

- VOO – tracks the S&P 500 (500 of the largest U.S. companies)

- QQQ – tracks major technology companies in the Nasdaq

- SCHD – focuses on high-quality dividend companies

The advantage is diversification.

Diversification means spreading investments across many companies so that no single failure destroys your portfolio.

ETFs tend to be:

- stable

- low-cost

- diversified

- easy to hold long term

They might not deliver explosive returns like the best growth stocks, but they also reduce the risk of catastrophic losses.

For many investors, ETFs become the foundation of their portfolio.

5. The “Cash Flow Machine”: Covered Call ETFs

Now we arrive at a newer and more controversial strategy: Covered Call ETFs.

These funds still hold stocks, similar to traditional ETFs.

But they add another layer: options trading.

Specifically, they sell covered call options.

Without getting overly technical, here’s the simplified explanation:

The ETF allows other investors the right to buy certain stocks at a future price.

In exchange, the ETF collects a premium (a fee).

That premium becomes income, which the ETF distributes to shareholders.

Because of this strategy, some covered call ETFs can generate very high yields, sometimes in the 10–15% range or higher.

Examples include:

- TSPY – a covered call strategy based on the S&P 500

- QQQI – a covered call strategy based on the Nasdaq-100

Many of these funds pay monthly dividends, which is attractive for income-focused investors.

However, there are trade-offs.

Covered call strategies often limit upside gains when markets rise quickly.

There is also a risk known as NAV erosion.

NAV (Net Asset Value) represents the underlying value of the ETF’s assets. If the fund consistently pays large distributions while its price steadily declines, investors may be receiving their own capital back, rather than true investment profits.

Because many covered call ETFs are relatively new, their long-term track record is limited.

So investors should proceed thoughtfully.

Why Smart Investors Use Multiple Strategies

Here’s an important truth about investing:

No single strategy solves everything.

Each one serves a different purpose.

A balanced approach might look like this:

Savings accounts → emergency liquidity

Growth stocks → long-term wealth creation

Dividend stocks → steady income

ETFs → diversification and stability

Covered call ETFs → enhanced cash flow

Instead of choosing just one approach, many investors combine them.

My Current Investing Curiosity

Recently I’ve been fascinated by covered call ETFs like TSPY and QQQI.

Why?

Because they generate monthly income.

Right now, some yields are around 14–15% annually, paid monthly.

Imagine this scenario:

You receive dividend income every month.

Instead of spending it, you reinvest it into:

- growth stocks

- ETFs

- dividend stocks

Now your investments are generating more investments.

This creates a powerful force called compounding.

Compounding happens when returns generate additional returns, creating exponential growth over time.

In simple terms:

Money makes money…

and that money makes even more money.

That’s when investing starts to feel less like saving—and more like building a financial machine.

The Big Takeaway

Saving money is important.

But where you put that money matters even more.

Some strategies protect your money.

Some grow it.

Some generate income.

The real goal is finding the mix that helps your money work as hard as you did to earn it.

Related Articles:

Financial and Legal Disclaimer

The content provided on HelpYourFinances.com is intended for general informational purposes only and does not constitute financial, legal, or professional advice. While we make every effort to ensure the accuracy and reliability of the information presented, it is important to understand that financial and legal matters are complex and highly individual.

HelpYourFinances.com is not a licensed financial planner, investment advisor, legal professional, or law firm. The materials on this website should not be considered a substitute for personalized advice from qualified financial advisors, attorneys, or other licensed professionals who can assess your unique situation.

Before making any financial, legal, or other important decisions, we strongly encourage you to seek advice from qualified experts. Any reliance you place on the information provided here is strictly at your own risk. HelpYourFinances.com, its owners, and contributors disclaim any liability for actions taken based on the content of this website.