Cars are not investments.

They are depleting assets — financial objects that slowly fall apart every time you use them.

Every mile driven:

- Tires lose tread

- Brakes inch closer to replacement

- Something, somewhere, is aging faster than it should

Eventually, the car gives you the look:

“It’s been real. I’m done.”

That moment should not come with panic, debt, or financial gymnastics. The solution is simple but often ignored:

👉 You need a Car Fund.

Why a Car Fund Matters

If you know you’ll replace a car every few years — and that replacement costs around $25,000 — the mistake isn’t the purchase.

The mistake is not planning for it.

Let’s assume the following:

- Monthly budget: $500

- Target purchase: $25,000 used car

- Annual income: $150,000

- Existing brokerage account: $100,000

- Goal: Replace a car without disrupting long-term wealth

The question isn’t if you’ll buy another car.

The question is:

What’s the smartest way to fund it?

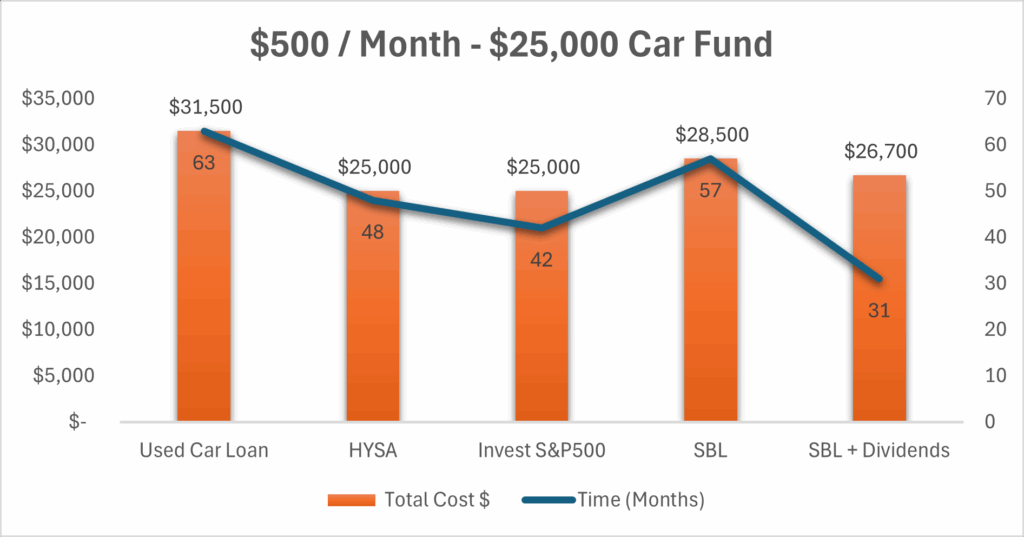

Scenario 1: Used Car Loan (With a $500/Month Cap)

How it works:

You finance a $25,000 used car but cap payments at $500/month, because that’s the budget — not a suggestion.

Loan assumptions

- Loan amount: $25,000

- Interest rate: ~7% (typical used car rate)

- Monthly payment: $500 (fixed cap)

What the math actually says

With a $500/month payment at 7%:

- Payoff time: ~63 months

→ Just over 5 years - Total paid: ~$31,500

- Total interest: ~$6,500

And remember — this entire time:

- The car is depreciating

- Repairs are increasing

- The loan balance declines slowly early on

You’re paying interest longer than the typical ownership cycle of a used car.

Taxes & opportunity cost

- Interest is not tax-deductible

- Cash flow is locked into a depreciating asset

- Money cannot be redirected to investing or saving during those 5+ years

Why this matters

The issue isn’t just cost — it’s duration.

You’re still paying for the car when:

- The resale value has collapsed

- The next replacement cycle is already approaching

Verdict

❌ Still ruled out — but now for better reasons

Scenario 2: High-Yield Savings Account (Safe and Predictable)

How it works:

Save $500/month in a high-yield savings account earning ~4–5%.

Pros

- No market risk

- Fully liquid

- Predictable outcome

Cons

- Modest growth

- Interest taxed as ordinary income

Real-world outcome

Saving $500/month for ~4 years at ~4.5%:

- Ending balance: ~$26,000–$27,000

At a $150,000 income:

- Interest taxed around 24%

- After-tax return closer to ~3–3.5%

Verdict

✅ The “sleep-well-at-night” option

Not exciting, but extremely reliable.

Scenario 3: Investing the Car Fund in an S&P 500 ETF

How it works:

Invest $500/month into a broad market ETF and sell when ready to buy the car.

Pros

- Historically higher returns (8–10% long-term)

- Strong chance of reaching $25,000 faster

Cons

- Market volatility

- Timing risk if the market drops when you need the cash

Taxes

- No tax while invested

- Upon sale:

- 15% long-term capital gains tax if held over one year

Verdict

⚖️ Best expected return, but requires discipline

Works best if money is shifted to cash 6–12 months before purchase.

Scenario 4: Securities-Backed Loan (SBL)

How it works:

Borrow against your existing $100,000 brokerage account instead of selling investments.

Assumptions:

- Loan amount: $25,000

- Interest rate: ~7%

- Monthly payment: $500

Outcome

- Payoff time: ~4.75 years

- Total interest: ~$3,500

Pros

- No need to sell investments

- No capital gains triggered

- Flexible repayment

Cons

- Market risk

- Interest is not tax-deductible

- Portfolio declines can create pressure

Verdict

⚠️ Effective, but not beginner-friendly

A tool — not a default.

Scenario 5: Securities-Backed Loan + Dividends (The Wealthy Person Move)

This is where strategy replaces brute force.

How it works:

You take the same $25,000 SBL — but now you use dividends from your investments to accelerate payoff on top of the $500/month budget.

Updated assumptions

- Brokerage account: $100,000

- Dividend yield: 5% annually

- Annual dividends: ~$5,000

- Monthly dividends: ~$417

- Dividends are fully applied to the loan

Payment power

- $500 (cash flow)

- ~$417 (dividends)

- = ~$917/month effective payment

Payoff impact

- Loan paid off in ~30–32 months (~2.5 years)

- Total interest drops to ~$1,500–$1,700

Tax reality

- Qualified dividends taxed at ~15%

- After-tax dividends ≈ ~$354/month

- Even after tax:

- Effective payment ≈ $850+/month

- Payoff still ~33–35 months

Opportunity cost

- Dividends are not reinvested

- But you earn a guaranteed 7% return by eliminating interest

- Reduced leverage risk faster

Verdict

✅ The most efficient strategy if you already have assets

You’re letting your money work while you sleep — and while you drive.

Final Takeaway: The Smart Car Fund Hierarchy

❌ Avoid

- Used car loans that break your monthly budget

✅ Solid choices

- HYSA for certainty

- S&P 500 ETF for growth with timing discipline

🚀 Advanced strategy

- SBL + dividends for faster payoff and lower interest

The Real Lesson

Cars are unavoidable.

Debt panic is optional.

The financially disciplined don’t ask:

“What can I afford monthly?”

They ask:

“How do I replace a depreciating asset without sabotaging my future?”

That’s what a car fund does.

It doesn’t make cars exciting —

it makes them irrelevant to your long-term wealth.

And that’s the ultimate flex. 🚗💰

Related Articles:

Financial and Legal Disclaimer

The content provided on HelpYourFinances.com is intended for general informational purposes only and does not constitute financial, legal, or professional advice. While we make every effort to ensure the accuracy and reliability of the information presented, it is important to understand that financial and legal matters are complex and highly individual.

HelpYourFinances.com is not a licensed financial planner, investment advisor, legal professional, or law firm. The materials on this website should not be considered a substitute for personalized advice from qualified financial advisors, attorneys, or other licensed professionals who can assess your unique situation.

Before making any financial, legal, or other important decisions, we strongly encourage you to seek advice from qualified experts. Any reliance you place on the information provided here is strictly at your own risk. HelpYourFinances.com, its owners, and contributors disclaim any liability for actions taken based on the content of this website.